6 Tips for Advisors Working with Same-Sex Couples

by Craig Iskowitz, Founder and CEO of Ezra Group

“Equality is the soul of liberty; there is, in fact, no liberty without it.” - Frances Wright, Scottish writer and feminist

As society collectively pushes for equality, leaders in every industry should be thinking about how inclusive policies will impact their day-to-day operations. Wealth management is no different and financial advisors should start educating themselves on how best to support clients who identify in different minority groups.

Same-sex couples often have more complicated financial planning issues than heteronormative couples due to the unique challenges they face around money management. A higher proportion of LGBTQ people consider themselves “spenders” and are less likely to own financial products, such as mutual funds or life insurance than the general population. Furthermore, there is evidence of a wage gap that leaves some gay and lesbian individuals earning less than heterosexuals.

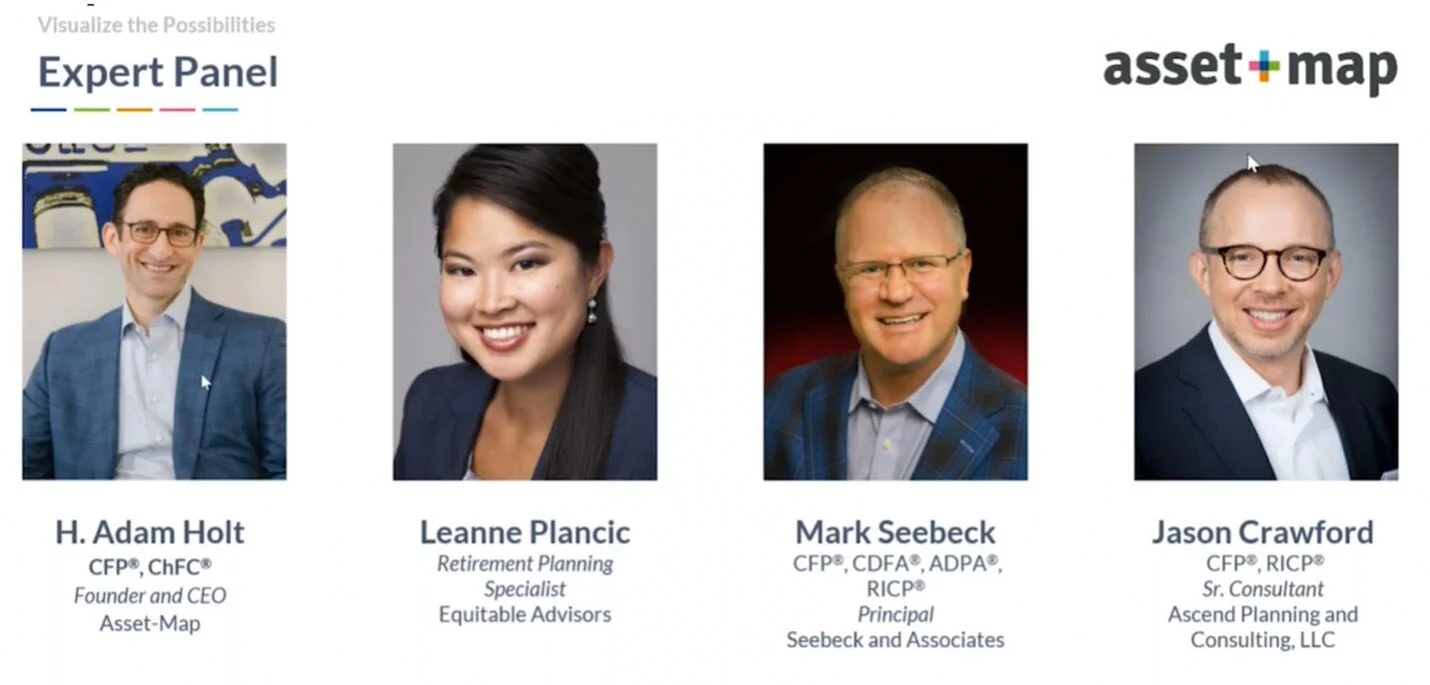

Asset-Map recently hosted a panel of financial planning experts to share insights for advisors on taking these differences into account when working with LGBTQ households. Here are six takeaways from the panel.

1. Don’t discount the difference

Advisors must be conscious not to assume that their same-sex clients are similar to straight ones.

“The term LGBTQ tells us how diverse even this small group of people is,” observed Mark Seebeck, Principal at Seebeck & Associates. “There are no two similar couples, but that is especially true in this community.”

Same-sex couples are less likely to be married than straight couples. Advisors need to be prepared to ask delicate questions such as who are the couple’s beneficiaries, or to which partner any shared children belong. Unmarried couples may not know how assets will be passed on and this is important to cover with clients who need to feel confident that their wills and other legal directives will be properly executed.

If the couple is unmarried or shares children who are only biologically related to one partner, power of attorney can also be more complicated. As Seebeck pointed out, “if your client doesn’t have power of attorney and their partner becomes unconscious, then critical decision-making could be assigned to a blood relative instead of them. This could potentially be someone your client is on bad terms with due to them not accepting their sexuality, and they may not care about your client’s well-being, only your client’s money.”

Leanne Plancic, Retirement Planning Specialist at Equitable Advisors, pointed out the sobering truth that while America has made progress on human rights, same-sex couples face still face problems in certain states that won’t recognize a queer partner as a relative.

When choosing who will represent them, Plancic asserts that same-sex clients will go with whoever takes their rights into account and fights for the values that make them who they are. Keeping inherent differences in mind will help advisors find, retain, and best support LGBTQ households.

2. Keep family planning top of mind.

Most people don’t know that there are additional costs associated with being gay in the US, specifically related to having children. Adoptions, surrogacy, and IVF in the case of transgendered couples can be very costly, creating difficulties for clients. It’s important to keep in mind that adoption, which costs an average of $43,000, can be subsidized by charities like HelpUsAdopt. They give grants of up to $15,000 towards children in need of families.

Some couples may opt for surrogacy, which comes with its own constraints. It’s illegal in four states, legally difficult in six, and comes with expensive legal bills in at least thirty. The average surrogacy costs come in between $90,000 and $130,000, which is a big line item on any couple’s financial plan.

Reciprocal IVF and insemination are slightly more budget-friendly, some health insurance plans will cover certain parts of the process. IVF can cost between $12,000 and $15,000 before hospital bills; additionally, insemination costs between $700 and $1,000 per attempt without the legal costs factored in.

When working with a younger same-sex couple, ask about whether they plan to have kids and how they plan to do so, and make adjustments based on the fertility option that best suits them. You may want to inquire about how they intend to cover childcare costs once their family starts to grow.

3. Take a look at their pay gap.

In a heteronormative relationship, we’re used to seeing men out-earn women by around 19%. The same kind of disparity also shows up in same-sex couples. According to Adam Holt, CEO of Asset-Map, there’s a common parallel where one partner earns more than the other, but there is not the same ability to transfer assets between partners as there is in a traditional union.

“One partner may have a powerful career and the other might be a stay-at-home spouse, or they may be in later relationships and have gone through a financial challenge in a previous relationship, leading them to start over,” Jason Crawford, Sr. Consultant at Ascend Planning and Consulting says of this. “It’s fine for individuals to plan independently of one another, but you need to have a clear understanding of both of their financial situations even if they’re not both clients.”

Financial advisors should aim to make sure clients have fair and equitable savings, which means if one partner is making much more than the other, they might still be able to save proportionally the same amount. If one partner considers themself a “spender” and the other more of a “saver,” discuss getting on the same page so that both parties are equally equipped for an unpredictable future.

4. Start adjusting for retirement costs early.

Many straight couples plan to lean on their children for support during retirement. As fewer LGBTQ couples have children, this might not be an option. Financial advisors should keep this in mind when creating a portfolio, adjusting retirement costs accordingly. Same-sex couples may want to save for a retirement home or unexpected medical bills.

“When the paychecks stop, they need to find new paychecks to supplement their retired lifestyles,” Crawford said during the panel. “Between retirement and death, all couples could expect to pay up to $200,000 dollars just in out-of-pocket expenses, and that’s important to put on an Asset-Map so emergencies don’t overwhelm clients.”

5. Take an introspective look at your value as an advisor.

Wall Street Traders have become a thing of the past with the rise of automation; financial advisors may find themselves similarly phased out if they aren’t prepared. Robo-advisors, which cost clients a quarter of the price of human advisors, are gaining market share. Seebeck asserts that this means advisors need to take a hard look at what they’re providing.

“The human aspect of being able to listen to peoples’ situation and life experiences makes their service something that stands out,” Seebeck commented. “Many LGBTQ couples are just looking for acceptance, but there will be some who look for this additional understanding of how it’s more expensive to be a gay person in the US.”

If financial advisors don’t want to repeat the past mistakes of travel agents - hello, Tripadvisor - they will need to adapt to suit the changing desires of their clients. When it comes to working with same-sex couples, doing your research, assessing their unique needs, and sprucing up your offerings to better support their niche will serve you in the long-run.

6. Cover the “in the case of death” questions, however uncomfortable

When talking to LGBTQ clients, legacy, as in who they’d like to own their assets once they’re gone, is especially important. The unfortunate reality means that a lot of queer people end up distanced from families who don’t accept them. Advisors need to ask: “who do you want your money going to?”

“Not all same-sex couples want their money going to their spouse and instead may want some money to go to nieces and nephews they’re fond of it they don’t have kids of their own,” Mark reminded panel listeners.

Advisors need to tackle beneficiary designation head-on, ensuring any properties are properly titled, and ready to go to the right person. If you’re working with an all-female couple, they’re likely to lead longer lives and therefore have more expenses. The healthcare space has room to grow when it comes to equality, meaning LGBTQ people need to have personal funds to cover their medical expenses as they age.

In summary

As the value of traditional financial advisors versus robo-advisors comes into question, human advisors should be analyzing who they can competitively serve clients in every minority group. This includes same-sex couples, who face specific challenges.

As long as advisors keep these tips at front of mind - accounting for differences, planning around pay gaps, and thinking proactively about family planning, retirement, and death - they’ll set themselves up to offer advantageous services that are best suited to LGBTQ couples seeking someone who’s on their side.

Leads marketing strategy at Asset Map, focused on advisor growth and engagement.